By Elaine Floyd, CFP ®

If you have lost a spouse (condolences to you) and are between the ages of 60 and 70, it will be important for you to consider your Social Security claiming options.

If you are entitled to both a survivor benefit based on your spouse’s work record and a retirement benefit based on your own work record, you may be able to coordinate these benefits to maximum advantage. In some cases it makes sense to start the survivor benefit first and switch to your own retirement benefit later. In other cases it’s better to delay the survivor benefit and receive your own benefit in the meantime.

Rules

First, the rules. (We are using one gender here, but if you are a widower these rules apply to you too.)

- If your husband died during the marriage and you were married at least nine months—or if your ex-spouse to whom you were married over 10 years died after the divorce—you become eligible for a survivor benefit based on your former spouse’s earnings record. You can claim this benefit as early as age 60 (50 if disabled).

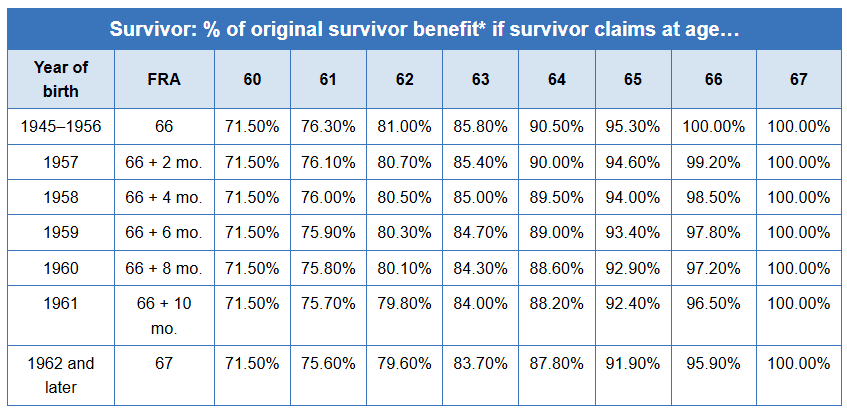

- At the time your spouse died the survivor benefit was set. This is called the “original” survivor benefit. (The “actual” benefit will depend on when you claim it—keep reading.) If your spouse had already claimed his benefit, the original survivor benefit will generally be the amount he was receiving at his death. If he had not yet claimed, the survivor benefit will generally be his Primary Insurance Amount (PIA) or the amount he would have received if he had lived to claim at his full retirement age (FRA).

- Your actual survivor benefit will be some percentage of the original survivor benefit depending on when you claim it. If you start it at your FRA you’ll get the full amount. If you start it anywhere between 60 and 67, you’ll get somewhere between 71.5% and 100% of the original benefit. Claiming the survivor benefit after FRA will not increase it.

- Your survivor benefit is independent of your own retirement benefit. The action you take with respect to one benefit will not affect the other. For example, if you start your survivor benefit at age 60, it will be reduced to 71.5% of the original benefit. If you later switch to your own retirement benefit, the reduction that was applied to the survivor benefit will not carry over to your retirement benefit.

- To receive a survivor benefit or a divorced-spouse survivor benefit you must be unmarried—or, if you have remarried, that marriage must have taken place after age 60.

- If you are under FRA and working, all benefits are subject to the earnings test: $1 in benefits will be withheld for every $2 earned over the annual threshold, which is $24,480 in 2026. This doesn’t necessarily mean you shouldn’t work or shouldn’t apply for benefits; more analysis is called for (see below).

Strategies

How do you know which benefit to start first? The first thing to do is find out the respective amounts. You’ll need to know your own PIA—that is, the amount of your retirement benefit if you claim it at your full retirement age of 67. You can find this on your latest Social Security statement (www.ssa.gov/myaccount). You’ll also need to know the amount of your survivor benefit. If your husband died after starting his benefit, your survivor benefit will generally be the amount of his benefit at the time of his death. If he died before starting benefits, you’ll need to call SSA (800-772-1213) to find out the amount of the survivor benefit. When you meet with an agent, be sure to get the amount of your survivor benefit if you were to claim it at your full retirement age. The Savvy Social Security Planning Software will make the necessary adjustments based on your claiming age.

You have two options when it comes to coordinating your two benefits.

Option 1.Start the survivor benefit first and switch to your own benefit at 70.

Option 2. Start your own benefit first and switch to your survivor benefit at FRA (67).

The key is to take the higher benefit last. By starting with the lower benefit and switching to the higher one, you can maximize your income in your later years.

Let’s look at some examples. In the first, the survivor benefit is higher than the widow’s own benefit will ever be. In the second, it’s reversed; if the widow delays her own benefit to age 70, she’ll end up with a higher amount than the survivor benefit. Once you have identified the highest potential benefit—by comparing the survivor benefit if taken at FRA to the retirement benefit if taken at 70—you want to preserve that benefit by taking it at the maximization age, which is FRA for the survivor benefit, 70 for the retirement benefit. With that stake in the ground you can go ahead and start the other benefit as early as possible even though it will be reduced.

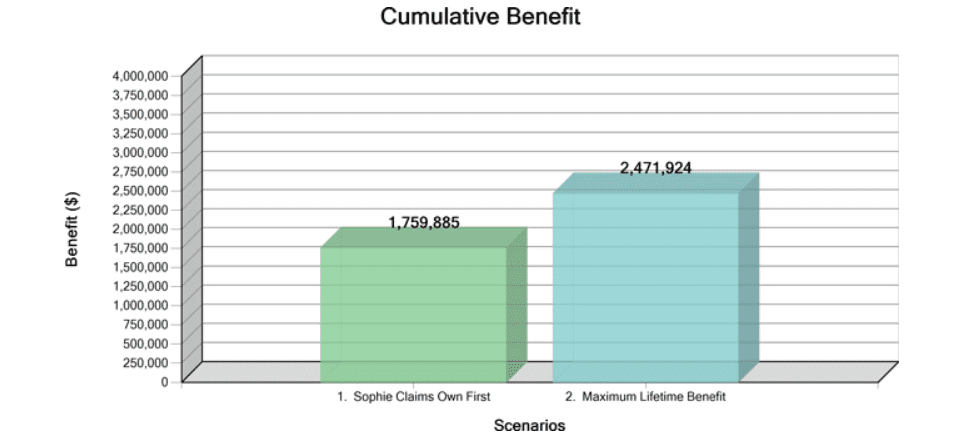

Sophie is a 60-year-old widow with a high earnings record. Her PIA is $3,600. Her deceased husband’s PIA was $3,000. If she starts her own benefit at 70, she’ll get $4,464 ($3,600 x 1.24, plus annual COLAs), so that’s what she plans to do. In the meantime, she can receive the survivor benefit. If she starts it at age 60, she’ll get $2,145 ($3,000 x .715) per month until age 70, when she will switch to the $4,464.

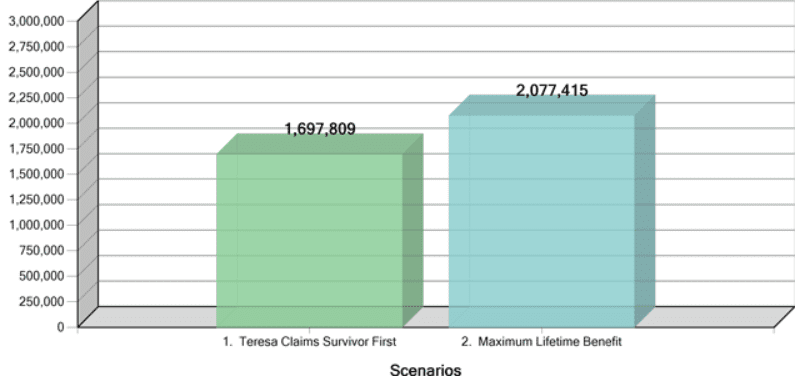

Teresa is a 60-year-old widow who was married to a high earner who died before starting benefits. According to his latest Social Security statement, his PIA was $3,800. Teresa also worked and has a PIA of $1,200. If Teresa takes the survivor benefit at FRA she will get $3,800 per month. This is higher than her own benefit will ever be. Even if she starts her own benefit at 70, with three years of 8% annual delayed credits she will get $1,488 ($1,200 x 1.24). The survivor benefit is higher, so she should hold out until FRA to take it. When she turns 62 she can start her own reduced retirement benefit, receiving $840 a month ($1,200 x .70) until she switches to the $3,800 survivor benefit at age 67.

Savvy Social Security Planning Analysis

The Savvy Social Security Planning Software takes into account your current age, your own PIA, the amount of the original survivor benefit—that is, the amount you would receive if you were to apply for it at your FRA—and your life expectancy.

The software shows your claiming options and identifies the one paying maximum benefits over your lifetime.

Here are Sophie’s options:

- Scenario 1: Sophie claims own benefit at 62 and switches to survivor benefit at 67.

- Scenario 2 (Maximum): Sophie claims survivor benefit at 60 and switches to own benefit at 70.

Clearly, she will receive more total benefits if she claims her survivor benefit first, at age 60, and switches to her own maximum benefit at 70.

Now let’s look at Teresa’s options.

- Scenario 1:Teresa claims survivor benefit at 60

- Scenario 2 (Maximum): Teresa claims own benefit at 62 and switches to survivor benefit at 67.

Teresa may be tempted (and may be advised by SSA) to take her survivor benefit as early as possible, at age 60. But this would cause it to be reduced to 71.5% of the full amount. This would be her permanent benefit. The better option for her would be to start her own reduced retirement benefit at 62 and switch to the maximum survivor benefit at 67. This will give her considerably more income from age 67 on and, if she lives to age 95, more total benefits over her lifetime (assuming 2% annual cost-of-living adjustments).

How to apply

The claiming strategy you decide upon will determine the application process. If you are applying for the survivor benefit and letting your own benefit grow to age 70 (like Sophie), you will need to make an appointment at your local Social Security office to apply for your survivor benefit. It is not possible to apply for survivor benefits online. Furthermore, you will need to tell the agent that you are restricting the scope of your application to your survivor benefit. Otherwise they might take an application for your own retirement benefit and this would stop the accumulation of delayed credits. Just say, “I do not wish this application for survivor benefits to be considered an application for retirement benefits on my own earning’s record.”

If you are applying for your own retirement benefit first (like Teresa), you can do so online. It will be a straight application for retirement benefits. SSA may not even notice that you also qualify for survivor benefits, but if they do you’ll want to make it clear that you are not applying for the survivor benefit at this time.

What about the earnings test?

The Savvy Social Security Planning Software does not take into account the earnings test, but if you are under FRA and working, whether you are receiving your survivor benefit or your retirement benefit, $1 in benefits will be withheld for every $2 you earn over the annual threshold, which is $24,480 in 2026.

This is not necessarily a reason not to work or not to apply for benefits. Because you’ll be switching benefits it may make sense to go ahead and start one of the benefits before FRA even though you are working. The exception would be if you earn enough to have all of your benefits withheld for the earnings test. To do the calculation, take your annual earnings, subtract the threshold amount ($24,480 in 2026) and divide by 2. This is the amount that would be withheld. If it exceeds your annual benefit, it wouldn’t make sense to apply. But if you would get even a few checks it’s worth it to apply even though some of your benefits will be withheld.

For example, let’s say Sophie is still working and earning $70,000 a year. Subtracting $24,480 and dividing by 2 we get $22,760. This is the amount that would be withheld for the earnings test. Sophie’s total first-year benefit would be $2,145 x 12 = $25,740. So, she would end up with $2,980 for the year even after the earnings test ($25,740 – $22,760). Once she turns 67 the earnings test would no longer apply.

As director of retirement and life planning for Horsesmouth, Elaine Floyd helps advisors better serve their clients by understanding the practical and technical aspects of retirement income planning. A former wirehouse broker, she earned her CFP designation in 1986.